Guest “Shedding light on the Big Lie” by David Middleton

While most of my recent posts have focused on Biden’s lies about the oil & gas industry, there is one BIG LIE that has become so pervasive, that has effectively become common knowledge.

U.S. producers reluctant to drill more oil, despite sky-high gas prices

BY IRINA IVANOVAUPDATED ON: MARCH 25, 2022

Consumers battered by sky-high gasoline prices shouldn’t expect relief from the oil industry anytime soon.

Many oil and gas executives say they have little interest in increasing oil production — even at crude’s near-record prices, which make extraction very profitable for their companies.

The price of crude oil has been steadily rising since the start of last year. It hit $100 a barrel in March after Russia invaded Ukraine — the first time in 12 years it breached three digits.

At that price, oil companies would normally race to snap up land and drill new wells. But a sizable number of oil and gas executives are saying they won’t increase production at any price, according to a survey released this week by the Federal Reserve Bank of Dallas.

[…]

To be fair to the mainstream media, they are too stupid to understand the difference between not increasing production and maintaining capital discipline. This particular journalist totally misread the Dallas Fed’s survey. The survey did not find that “a sizable number of oil and gas executives are saying they won’t increase production at any price.”

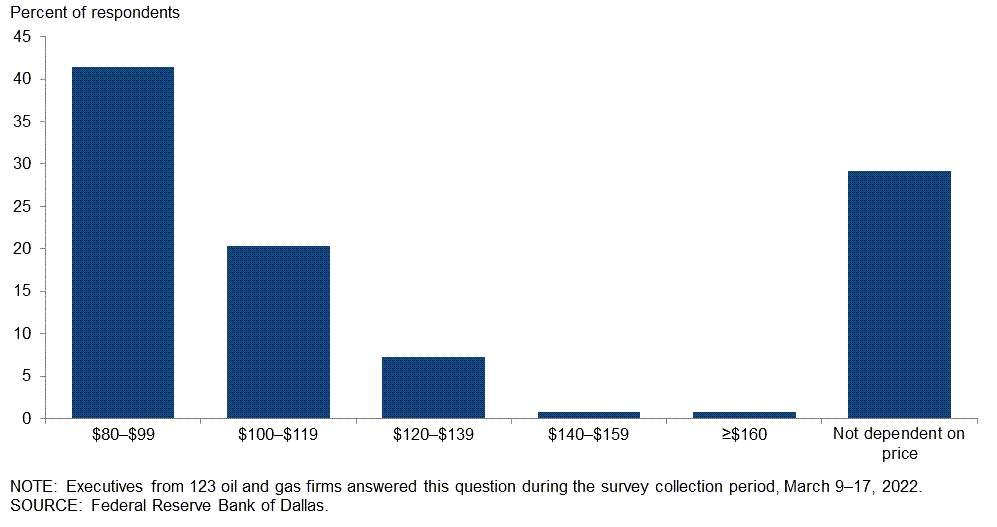

“What West Texas Intermediate crude oil price is necessary to get publicly traded U.S. producers back into growth mode?”

Dallas Fed

Saying that the decision to get “back into growth mode” isn’t dependent on price, isn’t even remotely close to “saying they won’t increase production at any price.” Firstly, oil companies can’t just flip a switch and increase production. Oil companies, have to increase capital expenditures (CapEx) and drill more wells in order to increase production. And… Guess what? Oil companies are increasing CapEx and drilling more wells. Secondly, getting “back into growth mode” is a 100% subjective phrase. Shrinking is sometimes a prerequisite for growth (shrink to grow).

CapEx

In my previous post, I focused in Pioneer Natural Resources Co. (PXD) because Biden specifically lied about what their CEO said about oil prices and increasing production. Today, I’ll expand it to include two other large independent “shale”-focused oil companies, EOG Resources Inc. (EOG) and Devon Energy Corp (DVN). First, let’s take a trip back to when “shale” was getting beaten up for not making big enough profits. Just prior to the onset of the shamdemic*, the “shale” sector actually started to generate free cash flow.

- Shamdemic: Pointless government-ordered economic lockdowns in response to ChiCom-19.

US SHALE INDUSTRY TURNS CASH FLOW POSITIVE

August 21, 2019In a remarkable turnaround, the second quarter of 2019 is the first three-month period on record when US shale operators achieved positive cash flow from operations after accounting for capital expenditures, according to Rystad Energy.

Rystad Energy – the independent energy research and consultancy in Norway with offices across the globe – has studied the financial performance of 40 dedicated US shale oil companies, focusing on cash flow from operating activities (CFO). This is the cash that is available to expand the business (via capital expenditure, or capex), reduce debt, or return to shareholders.

In the second quarter of 2019, 35% of operators in the peer group balanced their spending with operational cash flow, and reported an accumulated $110 million surplus in CFO versus capex.

[…]

I don’t have time (or the inclination) to try to recreate Rystad Energy’s “40 dedicated US shale companies,” but I did have the time to look at three of the larger independent “shale players”.

As can easily be seen on the chart above, the three companies roughly doubled their CapEx as the price of oil rose from $48 to $78/bbl. However, they did so in a financially disciplined manner. They not only maintained positive free cash flow, they grew their free cash flow as oil prices rose. They did exactly what they were bashed for not doing from 2008-2019. These companies will be releasing their Q1 2022 financials over the next few weeks. I’ll try to update this graph with those numbers.

Drilling

U.S. Oil Companies Have Increased Drilling By 60% In One Year

Robert Rapier Senior ContributorMar 27, 2022

One of the latest lines of attack in the finger-pointing over rising gasoline prices goes like this: U.S. oil companies are sitting on a huge number of permits, content to reap enormous profits while they refuse to drill for oil.

This is mostly false, but with a kernel of truth that is never taken in context. So let’s discuss what’s really happening.

The truth is that the number of rigs drilling for oil in the U.S. is steadily climbing. The year-over-year increase in the Baker Hughes North America Rig Count is now about 60%. In fact, historically it has rarely climbed at a faster pace than this. Clearly, the notion that oil companies are just sitting on their hands, content to withhold production and squeeze American consumers is false.

[…]

Finally — and here is the bit that contains a nugget of truth — many oil companies have said they are going to be more financially disciplined than they have been through previous boom and bust cycles.

Critics of the oil and gas industry have seized on this financial discipline as proof that oil companies are holding back production. However, one of the biggest criticisms about the shale boom over the past 15 years is that the oil companies never make consistent money. Indeed, if you look at the financials of many oil companies, they lost money in four of the past ten years.

[…]

I can assure you that each oil company wants to produce as much oil as they can at current prices, because they will indeed be very profitable with oil prices above $100/bbl. But they can’t immediately toggle production higher, and they don’t have crystal balls. They don’t know where oil prices will be a year or two from now, and that’s the reason you don’t see them ramping up drilling at an even faster pace.

You may disagree with their decisions, which is your right. But you should at least understand the reasons for these decisions.

As Mr. Rapier goes on to note, there is a lag time between drilling and production. However, oil companies are increasing CapEx and they are spending more money on drilling.

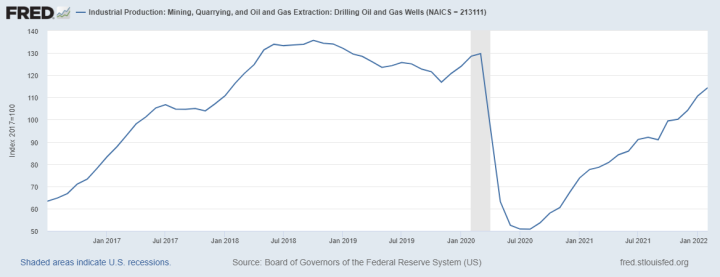

St. Louis Fed

While still below the pre-shamdemic peak, oil & gas drilling activity is growing at about the same pace as it was from 2017-2019.

Production

US crude oil production has been slowly rising. It’s currently about 1 million bbl/d higher than it was in September 2020. Although it’s still about 1.4 million bbl/d lower than it was just prior to the shamdemic*.

The most prolific oil play, the Permian Basin has already exceeded it’s pre-shamdemic* level.

Here is a zoomed in version of Permian Basin oil production (lower left panel):

Maybe if Biden hadn’t been unlawfully blocking lease sales and slow-walking permits, the second most prolific US oil producing region, the Gulf of Mexico, might be doing the same thing.

No Crystal Ball

After 41 years in the oil & gas industry, if I’ve learned one thing, it’s that almost all oil and natural gas price predictions are wrong.

We think gas prices will stay in this $9 to $11 range, there’ll be times like in July when they’re above it, there’ll be times when they’re below it and of course the weather will matter a lot as well. But we’re pretty confident that much below $9 you’d see a drop off in drilling activity particularly among the conventional drilling and then those pretty aggressive 35% to 40% first year declines are going to kick in and rebalance the market.

I saw something the other day where some analysts had come up with production in 2010 was going to be up by something like 8 to 10 BCF a day and gas prices were going to be $6.25. That kind of analysis I think can only come at the dangerous intersection of Excel and PowerPoint, it can’t happen in reality.

Chesapeake CEO Aubrey McClendon, August 1, 2008

NEW YORK (Reuters) – Texas oil billionaire T. Boone Pickens said on Thursday crude prices may soon fall as low as $110 a barrel amid falling gasoline demand, but should not sink below $100 because the United States depends heavily on oil imports.

“I don’t think it’ll drop below $100,” Pickens told Reuters in a telephone interview. “I would say $110 is where it might go, something like that.”

Needless to say, the late Aubrey McClendon’s and the late T. Boone Pickens’ predictions of permanently high oil & natural gas prices were wrong. This is not a criticism of either man. They were both brilliant oil & gas industry pioneers. They were just wrong.

We may not have a crystal ball, but we do have a futures market. Why would any sane oil company be spending money under the assumption that $100-$130/bbl oil was here to stay, when the same sorts of investors demanding financial discipline think oil prices will be back down in the $80’s next year?

via Watts Up With That?

April 5, 2022 at 04:41PM