Guest ridicule by David Middleton

This article is a follow-up to George Moonbat’s While economic growth continues we’ll never kick our fossil fuels habit,covered by Eric Worrall in this post: Monbiot: The Stimulus Effect of the Renewable Economy is Tempting Green Entrepreneurs to Fly More.

Too fracking funny! The pop-up ad is for Southwest Airlines!

Climate change and the true cost of economic growth

Readers respond to George Monbiot’s request to start a conversation about the links between climate breakdown and consumerism

If George Monbiot really wants to get people talking about the connection between climate change and the economy, he’d do better to find a different question to “how do we stop growth?” (While growth continues we’ll never kick our fossil fuel habit, 26 September).

The elephant in the room is the assumption that nature’s resources and capabilities are so large that they can be considered infinite and so excluded from the economic cost of production. This has the unintended consequence of rewarding destruction. Hence the German situation in Hambacher: the lignite has value because it can be sold to be burned, the 12,000-year-old forest has none unless the trees are cut down for economic use. And, in an infinite world, there are always more 12,000-year-old forests.

This form of thinking might have been a useful simplification when human population and activities were at the levels of the Enlightenment, when much of the philosophy that still drives the economy was developed. Indeed, for any one individual the world is still a remarkably big place and it is difficult to imagine it running out of anything. But a resource that would have supplied an Enlightenment-sized population for 500 years would last today’s just 35 years. And that is without considering increased rates of consumption.

[…]

We now have another new phrase for Gorebal Warming: Climate Breakdown

Here is a summary of the readers’ responses to Mr. Moonbat:

- Rewrite the laws of economics “to reward activities that nourish our future.”

- Make the UK more bicycle-friendly, like Holland.

- The BBC should stop ignoring climate change.

- Tell us how to practically “get from where we are to where we should be, without catastrophic unemployment, poverty and civil unrest.”

- “Stop driving fossil-fuel cars. Become vegetarian. Consume less. Use less energy…” ad nauseum.

- “A much simplified lifestyle: being happy with our personal relationships, reducing most forms of competition, and devoting our time to caring for other members of society…” double ad nauseum

- Reduce the human population… “but this obviously raises some unpleasant decisions.” Not if you’re a Vogon.

I won’t bother to ridicule the useful idiots (the readers whose comments were summarized above)… Unless calling them useful idiots is a form of ridicule… In which case I just ridiculed them.

Instead, I’ll focus on ridiculing the Grauniad’s idiotic preamble.

Warning: The rest of this post is a rather detailed discussion of resource economics.

“Climate change and the true cost of economic growth”

There is no “true cost of economic growth.” The cost of economic growth, including compliance with regulations, is built into the calculation of economic growth. To the extent that future climate change may or may not impact future economic growth, there’s no evidence that “carbon” regulations will do anything other than moving the costs back in time from the future to the present. A real-world discount rate zeroes out all potential “benefits” of carbon regulations.

How Climate Rules Might Fade Away

Obama used an arcane number to craft his regulations. Trump could use it to undo them.

by Matthew Philips , Mark Drajem , and Jennifer A Dlouhy

December 15, 2016, 3:30 AM CST

In February 2009, a month after Barack Obama took office, two academics sat across from each other in the White House mess hall. Over a club sandwich, Michael Greenstone, a White House economist, and Cass Sunstein, Obama’s top regulatory officer, decided that the executive branch needed to figure out how to estimate the economic damage from climate change. With the recession in full swing, they were rightly skeptical about the chances that Congress would pass a nationwide cap-and-trade bill. Greenstone and Sunstein knew they needed a Plan B: a way to regulate carbon emissions without going through Congress.

Over the next year, a team of economists, scientists, and lawyers from across the federal government convened to come up with a dollar amount for the economic cost of carbon emissions. Whatever value they hit upon would be used to determine the scope of regulations aimed at reducing the damage from climate change. The bigger the estimate, the more costly the rules meant to address it could be. After a year of modeling different scenarios, the team came up with a central estimate of $21 per metric ton, which is to say that by their calculations, every ton of carbon emitted into the atmosphere imposed $21 of economic cost. It has since been raised to around $40 a ton.

This calculation, known as the Social Cost of Carbon (SCC), serves as the linchpin for much of the climate-related rules imposed by the White House over the past eight years. From capping the carbon emissions of power plants to cutting down on the amount of electricity used by the digital clock on a microwave, the SCC has given the Obama administration the legal justification to argue that the benefits these rules provide to society outweigh the costs they impose on industry.

It turns out that the same calculation used to justify so much of Obama’s climate agenda could be used by President-elect Donald Trump to undo a significant portion of it. As Trump nominates people who favor fossil fuels and oppose climate regulation to top positions in his cabinet, including Oklahoma Attorney General Scott Pruitt to head the Environmental Protection Agency and former Texas Governor Rick Perry to lead the Department of Energy, it seems clear that one of his primary objectives will be to dismantle much of Obama’s climate and clean energy legacy. He already appears to be focusing on the SCC.

[…]

The SCC models rely on a “discount rate” to state the harm from global warming in today’s dollars. The higher the discount rate, the lower the estimate of harm. That’s because the costs incurred by burning carbon lie mostly in the distant future, while the benefits (heat, electricity, etc.) are enjoyed today. A high discount rate shrinks the estimates of future costs but doesn’t affect present-day benefits. The team put together by Greenstone and Sunstein used a discount rate of 3 percent to come up with its central estimate of $21 a ton for damage inflicted by carbon. But changing that discount just slightly produces big swings in the overall cost of carbon, turning a number that’s pushing broad changes in everything from appliances to coal leasing decisions into one that would have little or no impact on policy.

According to a 2013 government update on the SCC, by applying a discount rate of 5 percent, the cost of carbon in 2020 comes out to $12 a ton; using a 2.5 percent rate, it’s $65. A 7 percent discount rate, which has been used by the EPA for other regulatory analysis, could actually lead to a negative carbon cost, which would seem to imply that carbon emissions are beneficial. “Once you start to dig into how the numbers are constructed, I cannot fathom how anyone could think it has any basis in reality,” says Daniel Simmons, vice president for policy at the American Energy Alliance and a member of the Trump transition team focusing on the Energy Department. “Depending on what the discount rate is, you go from a large number to a negative number, with some very reasonable assumptions.”

[…]

This is worth repeating:

A 7 percent discount rate, which has been used by the EPA for other regulatory analysis, could actually lead to a negative carbon cost, which would seem to imply that carbon emissions are beneficial.

OMB’s Whitewash on the Social Cost of Carbon

JULY 9, 2015

The “social cost of carbon” (SCC) is a key feature in the debate over climate change as well as the principal justification for costly regulations by the federal government. We here at IER and other critics have raised serious objections to the procedure by which the Obama Administration has produced estimates of the SCC.

Last summer I did a post on the GAO’s whitewash of our criticism, and now—just before the Independence Day holiday weekend—the Office of Management and Budget (OMB) has released its own whitewash.

There are several key points on which the Administration is obfuscating, but in this post I’ll focus just on the choice of discount rates. This one variable alone is sufficient to completely neuter the case for regulating carbon dioxide emissions using the social cost of carbon, so it is crucial to understand the controversy.

[…]

Why Do We Discount Future Damages?

Present dollars are more important than future dollars. If you have to suffer damage worth (say) $10,000, you will be relieved to learn that it will hit you in 20 years, rather than tomorrow. This preference isn’t simply a psychological one of wanting to defer pain. No: Because market interest rates are positive, it is cheaper for you to deal with a $10,000 damage that won’t hit for 20 years. That’s because you can set aside a smaller sum today and invest it (perhaps in safe bonds), so that the value of your side fund will grow to $10,000 in 20 years’ time.

In this framework, it is easy to see how crucial the interest rate is, on those safe bonds. If your side fund grows at 7% per year, then you need to set aside about $2,584 today in order to have $10,000 in 20 years. But if the interest rate is only 3%, then you need to put aside $5,537 today in order to have $10,000 to pay for the damage in 20 years.

An equivalent way of stating these facts is to say that the present-discounted value of the looming $10,000 in damages (which won’t hit for 20 years) is $2,584 using a 7% discount rate, but $5,537 using a 3% discount rate. The underlying assumption about the size and timing of the damage is the same—the only thing we changed is the discount rate used in our assessment of it.

Discount Rates in Climate Policy

Generally speaking, the climate damages that occur in computer simulations don’t begin to significantly affect human welfare in the aggregate until the second half of the 21st century. In other words, the computer-simulated damages need to be discounted over the course of decades and even centuries. (The Obama Administration Working Group used three computer models to calculate damages through the year 2300.) Thus we can see why the choice of discount rate is so crucial.

In its latest revision, the Working Group estimated that for an additional ton of carbon dioxide emitted in the year 2015, the present-value of future net damages would be $11 using a 5% discount rate, $36 using a 3% rate, and $56 using a 2.5% rate (see table on page 3 here). Yet when the media refer to these numbers as “the social cost of carbon,” it obscures how arbitrary the figures are. They can range from $11/ton to $56/ton just by adjusting the discount rate in a narrow band from 5% to 2.5%.

Violating OMB’s Clear Guidance

Fortunately, OMB provides explicit guidance (in the form of “OMB Circulars”) to federal agencies on how to select discount rates. Specifically, as we carefully explain on pages 12-17 of IER’s formal Comment, OMB Circular A-4 (relying in turn on Circular A-94) states that “a real discount rate of 7 percent should be used as a base-case for regulatory analysis,” as this is the average before-tax rate of return to private capital investment.

Now it’s true, Circular A-4 goes on to acknowledges that in some cases, the displacement of consumption is more relevant to assess the impact of the policy under consideration, in which case a real discount rate of 3 percent should be used. Thus it states: “For regulatory analysis, you should provide estimates of net benefits using both 3 percent and 7 percent” (bold added).

[…]

As a default position, OMB Circular A-94 states that a real discount rate of 7 percent should be used as a base-case for regulatory analysis. The 7 percent rate is an estimate of the average before-tax rate of return to private capital in the U.S. economy…

Figure 3 from Nordhaus (2017), modified by author. A linear extrapolation of Nordhaus’ discount rate plot implies that a 7% discount rate would zero-out the social cost of carbon.

Application of a 7% discount rate makes the Social Cost of Carbon…

Dean Wormer just never gets old!

Reference

Nordhaus, William D. Revisiting the social cost of carbon. PNAS 2017 114 (7) 1518-1523; published ahead of print January 31, 2017, doi:10.1073/pnas.1609244114

“The elephant in the room is the assumption that nature’s resources and capabilities are so large that they can be considered infinite and so excluded from the economic cost of production.”

This notion is mind-boggling in its idiocy.

Depletion is very much not “excluded from the economic cost of production.” The depletion rate is integral to the economics of all mining and resource extraction industries.

That said, most of “nature’s resources and capabilities are so large that they can be considered infinite” from a human perspective. This doesn’t mean that we should exploit them wantonly. Effective exploitation requires that they be produced efficiently, in order to maximize production

Time and space don’t permit me to examine all of “nature’s resources”… But since I’ve already examined a few of them…

The Five Metals of the Simon-Ehrlich Wager

This is from a post of mine in 2012 on the Simon-Ehrlich wager:

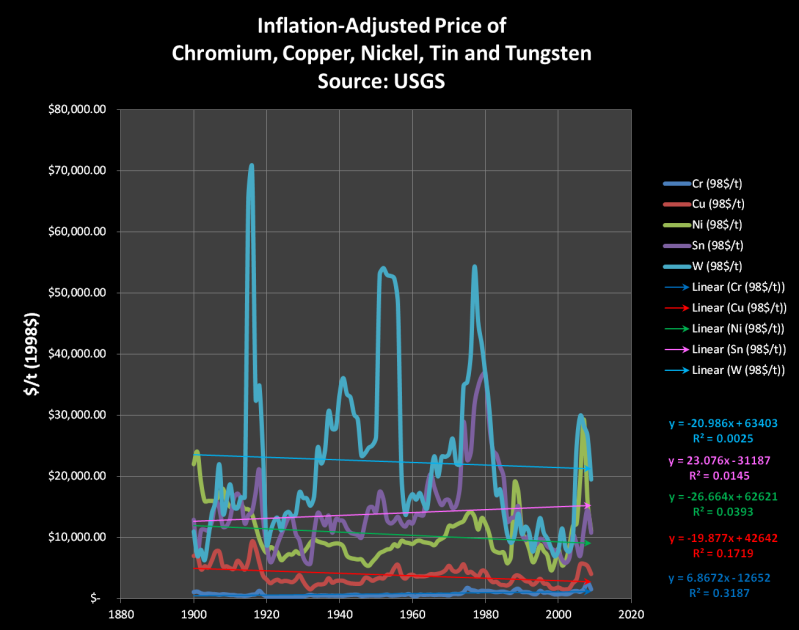

Rather than “cherry-picking” particular decades, I took a look at the full historical price record (available from the USGS). The inflation adjusted prices of Chromium (Cr), Copper (Cu), Nickel (Ni), Tin (Sn) and Tungsten

exhibit no statistically meaningful inflation-adjusted price trend over the last 110 years…

Cu, Ni and W have slightly negative slopes; while Cr and Sn have slightly positive slopes… Only chromium’s (R^2 = 0.3187) and copper’s (R^2 = 0.1719) trend lines approach statistical significance.

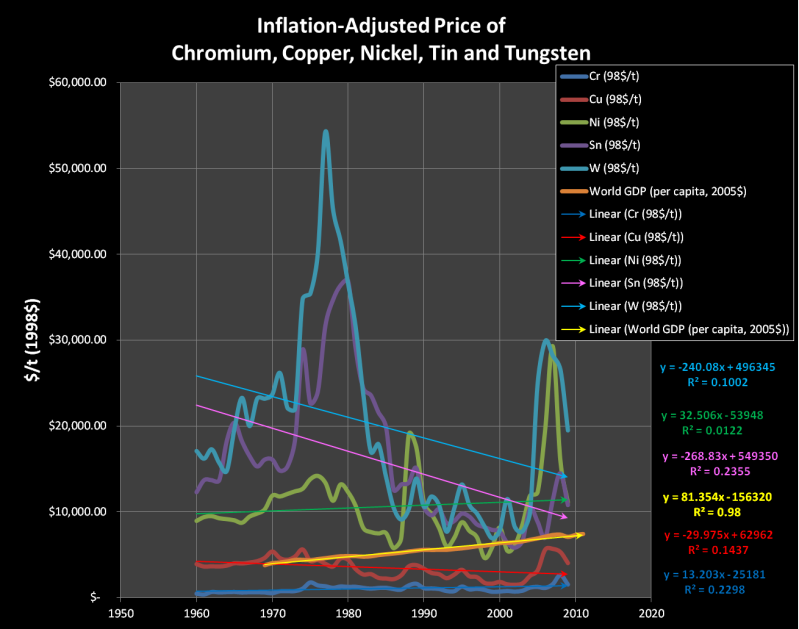

While the inflation adjusted price of these metals is a good measure of affordability, it is not a complete measure. The price is only relevant if it is measured against the financial resources available. Relative to world real per capita GDP all five metals have become more affordable since 1969…

The GDP slope is positive and highly statistically significant (R^2 = 0.98). The GDP slope (81.354) is almost three times larger than the largest positive metal slope (Ni, 32.506).

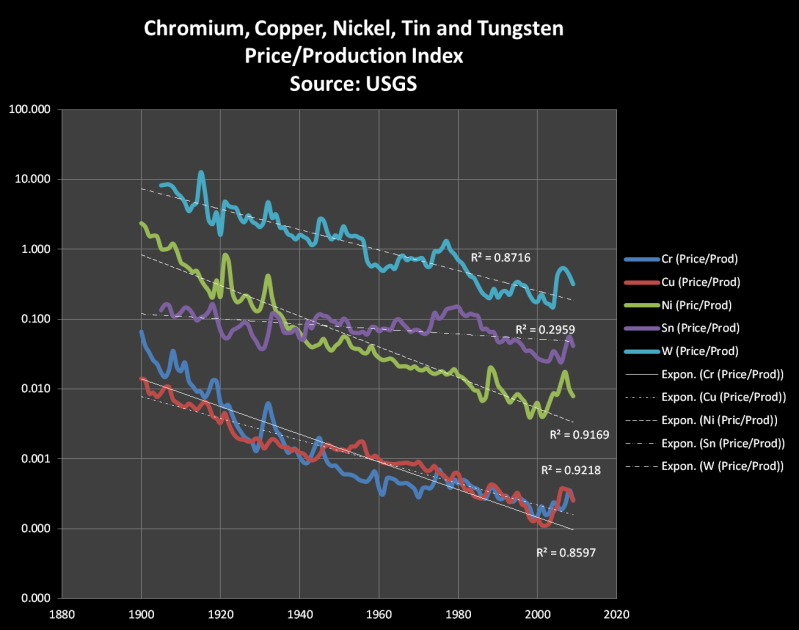

More importantly, from a scarcity perspective, the production output of all five metals has been rising over time. Four are rising exponentially …

While the ratio of price to output has been declining exponentially…

If these metals were becoming more scarce, the price would be rising faster than the supply.

The USGS estimates that the current proved reserves of all five metals are sufficient to meet demand for the next 20 to 59 years. For “fun” I estimated the crustal mass of all five metals and estimated how long it would take to literally run out at the current production rate…

Even with the “meteoric” rise of electric vehicles, I’m pretty sure that the five metals on the Simon-Ehrlich wager are still abundant and relatively affordable. Funny thing, one of the Warmunists’ favorite saviors from climate changes is the electric vehicle… This is from a post of mine on Halloween 2017…

Cobalt Cliffs and Lithium Landslides

In my previous post, we visited the “Cobalt Cliff“… an impenetrable obstacle standing in the way of Tesla building 500,000 Model 3 vehicles in 2018. Of course, now it appears that Tesla won’t have to worry about the cobalt cliff anytime soon. However, a cobalt cliff is out there, as is a lithium landslide.

The USGS is a great source for data on mineral production, proved reserves and resources.

Historical Statistics for Mineral and Material Commodities in the United States

The UBS article included a graphic of incremental metals demand in a 100% EV world. The graphic was reproduced here:

The graph makes a very simplistic assumption: If all vehicles were currently VW Golf’s, how would it impact mineral commodities if they were all replaced with Chevy Bolt’s? Simplistic, but a useful exercise. I took the incremental increases of lithium, cobalt and rare earths and calculated the amount of material per vehicle based on 2015 mineral production and made the assumption that there are currently 1 billion passenger vehicles in the world. I then estimated the mineral commodities demand that UBS’s 2015-2015 EV production forecast would yield.

Figure 4. Projected US EV sales (UBS) and minerals demand 2014-2015.

Figure 5. Projected EV sales and minerals consumption as % of 2015 global proved reserves.

Figure 6. Projected EV-driven mineral demand relative to historical production. (Minerals data from USGS).

Figure 7. Same as Figure 6, with a logarithmic y-axis.

Electric vehicle aficionados and other “futurists” like to use the word “disruptive” a lot. To quote Inigo Montoya, “You keep using that word. I do not think it means what you think it means.” The increases in mineral production required for just 45.6 million EV’s would be rather disruptive.

Proved mineral reserves are not fixed numbers. They are generally the “P90” number. There is a 90% probability that the proved reserves can be economically recovered from existing, developed mineral deposits. The total resource potential is much higher than the proved reserves. However, companies generally try to replace their annual production to maintain, or preferably increase, their proved reserves.

If UBS’s global EV production forecast is accurate, lithium and cobalt production will have to roughly double relative to 2014. The cumulative consumption of lithium from 2014-2015 will be equivalent to 69% of 2015 proved reserves. Cobalt consumption will be equivalent to 47% of proved reserves. This sort of production is not impossible; but it will be highly disruptive, particularly since most cobalt production is a byproduct of copper and nickel mining. According to the IEA…

“In order to limit temperature increases to below 2 degrees Celsius by the end of the century, the number of electric cars will need to reach 600 million by 2040”.

600 million EV’s would consume 907% of the 2015 proved lithium reserves and 615% of the 2015 proved cobalt reserves. That’s a lot. That’s disruptive.

Historical Mineral Production + EV Consumption Lithium Cobalt Rare Earths 2015-2025 Totals (metric tons) 9,643,510 3,266,267 1,672,179 2015 Proved Reserves (metric tons) 14,000,000 7,000,000 120,000,000 % Consumed @ 45.6 million EV 69% 47% 1% % Consumed @ 90 million EV 136% 92% 3% % Consumed @160 million EV 242% 164% 5% % Consumed @ 600 million EV 907% 615% 18% % Consumed @ 1,000 million EV 1512% 1024% 31% 615% of 7,000,000 metric tons is over 43,000,000 metric tons. This not only exceeds the 2015 proved reserves of cobalt, it exceeds the identified terrestrial resource potential…

Identified world terrestrial cobalt resources are about 25 million tons. The vast majority of these resources are in sediment-hosted stratiform copper deposits in Congo (Kinshasa) and Zambia; nickel-bearing laterite deposits in Australia and nearby island countries and Cuba; and magmatic nickel-copper sulfide deposits hosted in mafic and ultramafic rocks in Australia, Canada, Russia, and the United States. More than 120 million tons of cobalt resources have been identified in manganese nodules and crusts on the floor of the Atlantic, Indian, and Pacific Oceans.

Mining manganese nodules from the seafloor sounds really cool and disruptive!

Petroleum, Natural Gas and Coal… Oh My!

Petroleum proved reserves and resources may not be infinite, but they are fracking YUGE…

Summarizing the bar chart above…

| Billions of barrels (Bbbl) | World | North America | % North America |

| Cumulative Production | 1,200 | 310 | 26% |

| Proved Reserves | 1,680 | 220 | 13% |

| Conventional Resource | 1,435 | 260 | 18% |

| Unconventional Resource | 2,815 | 1,700 | 60% |

| Total Resource | 4,250 | 1,960 | 46% |

| Reserves + Resource | 5,930 | 2,180 | 37% |

| Years @ 28.1 Bbbl/yr | 211 | 78 | |

| Reserves + Resource + Cum. Prod. | 7,130 | 2,490 | |

| % Consumed | 17% | 12% | |

| % Remaining in the Ground | 83% | 88% |

The world has only consumed about 17% of its estimated total petroleum resource potential. For every barrel of petroleum that has been produced and consumed there are about five barrels of petroleum remaining in the ground. Of course this will all change if proved reserves and resource potential continue to grow.

Crude Oil Proved Reserves = 47 years of current consumption. MBO = million barrels of oil. Bbbl = billion barrels of oil. BP 2018 Statistical Review of World Energy.

Natural Gas Proved Reserves = 19 years of current consumption. BCF = billion cubic feet of gas. TCF = trillion cubic feet of gas. 2018 BP Statistical Review of World Energy.

Of course, like petroleum, proved reserves of natural gas are just a fraction of the resource base.

In the chart below, proved and probable resources are equivalent to proved (P90, 1P) and probable (P50, 2P) reserves.

P50 probable reserves (1P+2P) are nearly three times that of P90 proved reserves.

U.S. natural gas proved & probable reserves and resources (Bcf). Source: EIA and NGSA

U.S. natural gas proved & probable reserves and possible resources in years of production. Source: EIA and NGSA

For coal, we’ll just rely on BP’s numbers for reserves…

Coal reserves

World proved coal reserves are currently sufficient to meet 134 years of global production, much higher than the R/P ratio for oil and gas

By region, Asia Pacific holds the most proved reserves (41% of total), split mainly between Australia, China and India. The US remains the largest single reserve holder (24.2% of total).

Methodology

Total proved reserves of coal are generally taken to be those quantities that geological and engineering information indicates with reasonable certainly can be recovered in the future from known deposits under existing economic and operating conditions.Total proved coal reserves are shown for anthracite and bituminous (including brown coal) and sub-bituminous and lignite.

Reserves-to-production (R/P) ratios represent the length of time that those remaining reserves would last if production were to continue at the previous year’s rate. They are calculated by dividing remaining reserves at the end of the year by the production in that year. The R/P ratios are calculated excluding other solid fuels in reserves and production.

R/P ratios are available by country and feature in the table of coal reserves. R/P ratios for the region and the world are depicted in the chart above and the Energy charting tool.

Coal reserve data is in million tonnes.

Source

Includes data from Federal Institute for Geosciences and Natural Resources (BGR) Energy Study 2017.

Coal resources are a bit more difficult to assess. However, they are fracking YUGE. The USGS has conducted a coal resource assessment for these United States since 1974.

How much coal is in the United States?

The amount of coal that exists in the United States is difficult to estimate because it is buried underground. The most comprehensive national assessment of U.S. coal resources was published by the U.S. Geological Survey (USGS) in 1975, which indicated that as of January 1, 1974, coal resources in the United States totaled 4 trillion short tons. Although more recent regional assessments of U.S. coal resources have been conducted by the USGS, a new national-level assessment of U.S. coal resources has not been conducted.

The U.S. Energy Information Administration (EIA) publishes three measures of how much coal is left in the United States, which are based on various degrees of geologic certainty and on the economic feasibility of mining the coal.

EIA’s estimates for the amount of coal reserves as of January 1, 2017, by type of reserve

- Demonstrated Reserve Base (DRB) is the sum of coal in both measured and indicated resource categories of reliability. The DRB represents 100% of the in-place coal that could be mined commercially at a given time. EIA estimates the DRB at about 476 billion short tons, of which about 69% is underground mineable coal.

- Estimated recoverable reserves include only the coal that can be mined with today’s mining technology after considering accessibility constraints and recovery factors. EIA estimates U.S. recoverable coal reserves at about 254 billion short tons, of which about 58% is underground mineable coal.

- Recoverable reserves at producing mines are the amount of recoverable reserves that coal mining companies report to EIA for their U.S. coal mines that produced more than 25,000 short tons of coal in a year. EIA estimates these reserves at about 17 billion short tons of recoverable reserves, of which 65% is surface mineable coal.

Based on U.S. coal production in 2016 of about 0.73 billion short tons, the recoverable coal reserves would last about 348 years, and recoverable reserves at producing mines would last about 23 years. The actual number of years that those reserves will last depends on changes in production and reserves estimates.

[…]

This should demonstrate the scale of how much coal there is just in these regionally United States…

The most recent resource estimate is 10 times the demonstrated reserve base, which is rough;y 10 times the recoverable reserves at producing mines… And… Despite generating nearly 30% of our electricity from coal, the producing mines have no difficulty supplying more than enough coal.

How Can Reserves Continue to Grow as Oil Production Increases?

People often question the fact that proved oil reserves continue to climb as we produce more oil. This is counter-intuitive to most people, largely because politicians, the media and most people do not comprehend the meaning of the word “reserves” or the phrase “proved reserves.”

The word “reserves” has a specific definition:

Reserves

According to the Society of Petroleum Engineers, reserves are “those quantities of petroleum claimed to be commercially recoverable by application of development projects to known accumulations under defined conditions.” Well, that clears things up, right? No? Well, to clarify, the SPE says petroleum quantities must fit four criteria to be classified as reserves. They must be (1) discovered through one or more exploratory wells, (2) recoverable using existing technology, (3) commercially viable, and finally (4) remaining in the ground. Sound okay? Good, because it gets more tricky from there. There are currently three classifications for reserves: proved, probably and possible. Here’s how they break down:

Proved reserves

are those with a “reasonable certainty” (a minimum 90% confidence) of being recoverable under existing economic and political conditions. We can discussed the differences between proved developed, proved undeveloped, etc. with a later post. However, it should be pointed out that proved reserves are the only reserves recognized by the U.S. SEC. This is why energy companies strive to get the latest technology and recovery methods recognized by the government, therefore increasing the chance of “reasonably” recovering oil and gas assets and therefore raising their reserves as well.Probable reserves

are petroleum and gas quantities with a 50% confidence level of recovery. Basically, you may be able to get some, you may not.Possible reserves

are quantities with a minimum 10% certainty of being produced. Basically, your long shot discoveries. Only gamble on these types of assets if your Magic 8-Ball tells you to. All right! That takes care of reserves! But what about resources?Resources

For those of you who have looked at on the market ads, you’ll spot this term a lot in the literature. So what is resources? Again, we turn to the SPE. There are two categories of resources: contingent and prospective. are quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations, but the projects are not yet considered mature enough for commercial development due to one or more contingencies. In other words, there’s a good idea of how much oil and gas is in the reservoir, but issues such as political and social events or even a lack of market prevent production. There can be a major oil discovery in the Congo right now. You want to risk getting shot to get to it? are quantities of petroleum estimated to be potentially recoverable from undiscovered accumulations by application of future development projects. These sorts of resources basically exist in the minds of marketing people. That’s not to say that they don’t exist in the real world as well, it just means that E&Ps are thinking of future oil and gas discoveries in new areas, based on upcoming technology and the discoveries made in similar formations worldwide. Okay! I hope that helps! Until next time, may the resource be with you. Live long and prospect.

Proved reserves is the minimum volume of oil that is expected to be produced from a well quantified reservoir. This is generally the P90 number: There is a >90% probability that the proved reserve volume will be produced. This is often called 1P. Probable reserves is the most likely volume of oil that is expected to be produced from a well quantified reservoir. There is >50% probability that the probable reserve volume will be produced. This is called 2P and it is actually the current assessment of the most likely volume that will be produced.

“Proved reserves” are just a tiny fraction of the petroleum resource. It is primarily an accounting measure used in the valuation of oil companies. Publicly traded US oil companies have to “book” proved reserves according to very strict SEC rules.

Here’s a very simplistic example of proved reserves (1P):

Since the well was drilled up-dip to a dry hole with an oil show, the entire volume can be booked as proved because the down-dip well has an oil-water contact.

Here’s a very simplistic example of proved plus probable reserves(2P)

In this scenario, the down-dip well has no oil show, just a wet sandstone. If there is geological or geophysical evidence (e.g. seismic hydrocarbon indicator “HCI”) demonstrating that the hydrocarbon column extends down-dip, the volume below the lowest known oil can be booked as probable reserves. Otherwise, it would have to be categorized as possible reserves.

In some cases, seismic HCI’s can be used to delineate proved reserves, particularly if HCI’s have a track record in the field and/or play of accurately defining hydrocarbon accumulations.

Since proved reserves (1P) represents the >90% estimate of the producible volume, during the initial years of production, proved reserves will generally grow. Most reserve additions don’t come from new discoveries. They are the result of well performance, reservoir management and extensions of existing fields.

Most reserve additions don’t come from new discoveries. They come from reservoir management and field development operations.

New discoveries are the brown curve at the bottom of the chart.

Recently Bloomberg put out a bar chart showing how the size of new oil discoveries has steadily shrunk over the past 70 years. Here’s that bar chart at the same scale as global crude oil production and reserve growth.

There’s an old saying in the oil patch: “Big fields get bigger.” The biggest field in the world, Saudi Arabia’s Ghawar oil field was discovered in 1948. When first discovered, the estimated ultimate recovery (EUR) was in the neighborhood of 60 Bbbl. It has produced over 65 Bbbl and it is estimated to have about 70 Bbbl remaining (EUR ~130 Bbbl). Half of Ghawar’s EUR was recognized at its discovery. Half of it, or more, will be the result of field development and reservoir management. The EUR for Ghawar is not particularly controversial. Prior to the 1980’s, Aramco was at least partially owned by a consortium of American oil companies. Relatively detailed pertophysical data for the Arab D reservoir are publicly available.

The Ghawar Oil Field is by far the largest conventional oil field in the world and accounts for more than half of the cumulative oil production of Saudi Arabia. Although it is a single field, it is divided into six areas. From north to south, they are Fazran, Ain Dar, Shedgum, Uthmaniyah, Haradh and Hawiyah. Although Arab-C, Hanifa and Fadhili reservoirs are also present in parts of the field, the Arab-D reservoir accounts for nearly all of the reserves and production.

The Ghawar Field was discovered in 1948. Production began in 1951 and reached a peak of 5.7 million barrels per day in 1981. This is the highest sustained oil production rate achieved by any single oil field in world history. At the time that this record was achieved, the southern areas of Hawiyah and Haradh had not yet been fully developed. Production was restrained after 1981 for market reasons, but Ghawar remained the most important oil field in the world. The production of the Samotlor Field in Russia was greater during the mid-eighties, but this was because production at Ghawar was restrained. Development of the southern Hawiyah and Haradh areas during 1994 to 1996 allowed production from the Ghawar Field to exceed 5 million barrels per day once again, more than Samotlor ever produced.

This remarkable production history is because of the enormous size of the Arab-D reservoir in the Ghawar Field. Alsharhan and Kendall (1986, Table 1) provide a figure of 693,000 acres for the productive area of the Ghawar Field. This represents a single, pressure-continuous reservoir. Cumulative production by year end 2000 was about 51 billion barrels of oil.

The anhydrite in the Upper Arab-D forms the seal for the 1,300-foot oil column in Ghawar. It is composed of sabkha evaporites and subaqueous evaporites with thin carbonate interbeds that can be traced for hundreds of kilometers. The anhydrite thickens to the south at the expense of the reservoir zones; the combined thickness remains relatively constant.

[…]

Using the petrophysical data from the Croft analysis, it’s very easy to get to an EUR of 130 Bbbl.

[Ghawar reserve calculations to be added later]

Can we trust the reserve numbers of Saudi Arabia, Iran, Venezuela, etc.?

Well,,, You certainly can’t treat them the same as the audited 1P and 2P reserves of publicly traded oil companies, but they’re probably fairly realistic 2P to 3P numbers. 3P is possible reserves (>10% probability).

Note how the proved reserves of some nations suddenly jumped in single years.

BP Statistical Review of World Energy June 2017

The big jump in Canada’s proved oil reserves was the 1998 decision to “book” its oil sands (AKA tar sands) as proved reserves, which had previously been assessed as uneconomic.

The decision of accounting 174 billion barrels (28×109 m3) of the Alberta oil sands deposits as proven reserves was made by the Energy Resources Conservation Board (ERCB), now known as the Alberta Energy and Utilities Board (AEUB).[6] Although now widely accepted, this addition was controversial at the time because oil sands contain an extremely heavy form of crude oil known as bitumen which will not flow toward a well under reservoir conditions. Instead, it must be mined, heated, or diluted with solvents to allow it to be produced, and must be upgraded to lighter oil to be usable by refineries.[6] Historically known as bituminous sands or sometimes as “tar sands”, the deposits were exposed as major rivers cut through the oil-bearing formations to reveal the bitumen in the river banks. In recent years technological breakthroughs have overcome the economical and technical difficulties of producing the oil sands, and by 2007 64% of Alberta’s petroleum production of 1.86 million barrels per day (296,000 m3/d) was from oil sands rather than conventional oil fields. The ERCB estimates that by 2017 oil sands production will make up 88% of Alberta’s predicted oil production of 3.4 million barrels per day (540,000 m3/d).[6]

The fivefold increase in oil prices from 1998 to 2007 made Canadian oil sands production profitable.

Analysts estimate that a price of $30 to $40 per barrel is required to make new oil sands production profitable.[2]

Note that uneconomic oil can and has been produced and sold… It just can’t be booked as proved reserves.

Saudi Arabia’s proved oil reserves also made a big jump in 1990. It has been speculated that this was due to Aramco’s decision to claim that probable reserves were proved. However independent audits, related to Aramco’s possible IPO indicate that their proved reserves are actually greater than the 260 Bbbl previously reported.

Venezuela’s proved reserves made a big jump in 2007, eventually surpassing Saudi Arabia with about 300 Bbbl of proved reserves. Presumably this was based on higher oil prices making the heavy oil of the Orinoco Fold Belt more economically recoverable. However, the Venezuela proved reserves are probably more analogous to possible reserves or contingent resources.

That said, Venezuela has a lot of technically recoverable oil…

The Orinoco Oil Belt Assessment Unit of the La Luna−Quercual Total Petroleum System encompasses approximately 50,000 km2 of the East Venezuela Basin Province that is underlain by more than 1 trillion barrels of heavy oil-in-place. As part of a program directed at estimating the technically recoverable oil and gas resources of priority petroleum basins worldwide, the U.S. Geological Survey estimated the recoverable oil resources of the Orinoco Oil Belt Assessment Unit. This estimate relied mainly on published geologic and engineering data for reservoirs (net oil-saturated sandstone thickness and extent), petrophysical properties (porosity, water saturation, and formation volume factors), recovery factors determined by pilot projects, and estimates of volumes of oil-in-place. The U.S. Geological Survey estimated a mean volume of 513 billion barrels of technically recoverable heavy oil in the Orinoco Oil Belt Assessment Unit of the East Venezuela Basin Province; the range is 380 to 652 billion barrels. The Orinoco Oil Belt Assessment Unit thus contains one of the largest recoverable oil accumulations in the world.

While international proved reserve numbers are generally not as robust as those of the US and other OECD nations, they are at least in the ballpark of probable reserves.

Conclusion

“The elephant in the room” is either the smallest elephant on record or it’s one big @$$ room.

References

BP 2018 Statistical Review of World Energy

Schenk C.J., Cook, T.A., Charpentier, R.R., Pollastro, R.M., Klett, T.R., Tennyson, M.E., Kirschbaum, M.A., Brownfield, M.E., and Pitman, J.K., 2009, An estimate of recoverable heavy oil resources of the Orinoco Oil Belt, Venezuela: U.S. Geological Survey Fact Sheet 2009–3028, 4 p.

via Watts Up With That?

October 2, 2018 at 02:16PM