“Dominion has proposed a lower utilization rate (42.5%) than the Block Island because of the weaker winds off Virginia. The output from that project is already underperforming, and the records of other older wind farms in Europe confirm that wind farm utilization rates are often lower than initially assumed. Plus, the utilization rate declines as turbines age.”

On August 5, 2022, Virginia’s State Corporation Commission (SCC) approved the application by Virginia Electric and Power Company (Dominion Energy) to construct and operate the Coastal Virginia Offshore Wind (CVOW) project. Hearings on the nine-year-old proposed project have revealed numerous high-risk issues, any one of which could make costs skyrocket for customers. Instead, the SCC wants Dominion to shoulder one of them, causing Dominion to threaten to bail. Maybe it should for everyone’s sake.

Background

CVOW will consist of 176 turbines, each rated at 14.7 megawatts (MW) of generating capacity, creating a wind farm with a nameplate capacity of 2,587 MW. The wind turbines will be positioned on a federal lease held by VEP that lies 24 nautical miles off the coast of Virginia Beach, Virginia with underwater cables reading the shore.

The wind farm is scheduled to be fully operational by the end of 2026, at which time the company, under a SCC proposed condition, must achieve a “Performance Standard”—or else bear the cost rather than pass through costs to captive users.

This would be the first state energy plan that addresses the unlevel playing field enjoyed by renewable energy projects (more on this later), According to VEP’s filings, the total capital cost of the CVOW project is estimated to be approximately $9.8 billion, including approximately $1.15 billion for new and upgraded onshore Virginia facilities.

Total project costs over the life of the project, including financing costs, minus investment tax credits, are estimated to be approximately $21.5 billion. Over the project’s 35-year lifetime (including the five years for construction and the 30-year projected useful life), the company projects that a residential electricity customer using 1,000 kilowatt-hours (kWh) will see an average monthly bill increase of $4.72 and a peak monthly bill increase of $14.22 in 2027.

Dominion currently seeks to recover from customers in Rider OSW $78.7 million in costs associated with the project in its first year of construction.

Risk Factors

Here are the documented risk factors for Coastal Virginia Offshore Wind. One wonders if approval of this project will create the problems for Dominion that Plant Vogtle #3 and #4 have created for Georgia Power (Southern Company). Here are a dozen identified risks:

- As a first-mover project, there is no developed supply chain, including equipment suppliers, specialized installation vessels, and infrastructure to handle the transportation and installation of the equipment, which could lead to construction delays and cost overruns.

- Siemens Gamesa, the turbine supplier for the Project, has been “hit hard” by supply chain disruptions; this is further compounded by the fact that there are two installations ahead of the Project that will be receiving the same turbine designed by Siemens Gamesa.

- This type of project is not immune from general construction delays, For example, Ørsted A/S, the largest wind developer in the world, has experienced recent delays on projects in both Europe and the United States.

- The “fixed price” contracts for the Project provide for change orders, which can increase costs from those specified in the contracts.

- Higher-than-expected commodity prices, to the extent those prices have not been locked in, may lead to cost overruns.

- The final costs of necessary network upgrades with PJM Interconnection are unknown because ongoing study work in the PJM generation queue has stopped given the current backlog associated with issuing Facility Study Reports and Interconnection Service Agreements.

- The transmission interconnection facilities (i.e., Virginia Facilities) are a significant component of this Project, and the Company has experienced delays and cost overruns on recent transmission projects.

- Dominion’s cost projections do not specifically identify any costs it may seek to recover under Code § 56-585.1 A5e, which allows the Company to recover costs “necessary to mitigate impacts to marine life caused by construction of offshore wind generating facilities.”

- The Company’s rate of return on equity for the Project is not fixed and could increase in future years.

- For a project of this size and risk, the Company has only included a contingency estimate of approximately 3 percent, or $300 million.

- There is inherent risk associated with weather being more severe than expected during the construction and operational phase of the Project which may lead to construction delays and cost overruns.

- There is substantial evidence in the record addressing the significant operational risks attendant to this Project. The lifetime revenue requirement and levelized cost of energy estimates presented by the Company are based on a projection that CVOW, once in operation, will achieve a net 42% capacity factor. The lifetime revenue requirement for Rider OSW and the levelized cost of energy (“LCOE”) will increase if the actual achieved capacity factor is lower than projected.

Another risk identified by Walmart in its intervenor presentation was concerned a six-month weather window for the piling for offshore turbine foundations. Couple that restriction with possible bad weather, equipment operational issues, and availability of crews to operate the equipment, and there could be meaningful project delays that would inflate costs.

“Performance Standard” Condition

The Virginia State Corporation Commission has created a “performance standard” for CVOW that protects customers and shifts risks back onto Dominion. As outlined in the SCC decision:

- The Company based its cost-benefit analysis and LCOE proposal on an average net capacity factor of 42%, and Dominion continued to affirm its high level of confidence in relying upon a 42% capacity factor to undertake this Project. In short, the net capacity factor reflects the Project’s actual generation over a given period compared to the maximum amount it could have generated over that period.

- Based on the record herein, the Commission orders the required performance standard, beginning with commercial operation and extending for the life of the Project, customers shall be held harmless for any shortfall in energy production below an annual net capacity factor of 42%, as measured on a three-year rolling average.

Dominion CEO Robert Blue, in the company’s August 8 earnings call with investment analysts, called the performance standard “untenable.” He said it will likely lead Dominion to appeal the SCC’s ruling, or at least request a formal reconsideration. It is also possible that Dominion could sue the SCC over its approval decision citing it as creating a new condition, not within its purview.

A media article reporting on the SCC ruling noted how a Wall Street analyst had written that CVOW’s approval had been expected after agreements had been reached earlier this year between Dominion and various intervenors in the project’s application hearing. The performance standard provision was a “twist” that added uncertainty to the development of CVOW.

On the earnings call, Blue was asked if the performance standard could result in Dominion electing to “walk away from this project.” Because the company had only received the order on August 5 and it provided few details about the mechanics of the performance standard, Blue declined to give a specific response to the question.

As we look at it (the order), it is inconsistent with the utility risk profile expected by our investors. But it’s a great project and it has a lot of stakeholder support. There are options for us to seek reconsideration and options for us to work with stakeholders so that we can get that clarity that we need for this to meet our expectations of what utility investors are looking for.

The SCC outlined in the risks in light of the number of offshore wind projects ahead of CVOW that could result in delays/disruptions. This uncertainty about the CVOW’s status could also trigger costs from clauses in contracts for the project for delays.

With the Biden administration pounding the table for offshore wind projects to move forward as quickly as possible, there is a lineup of new projects awaiting construction, and any disruptions in the progress of earlier projects could be detrimental to the financial returns of later projects such as CVOW.

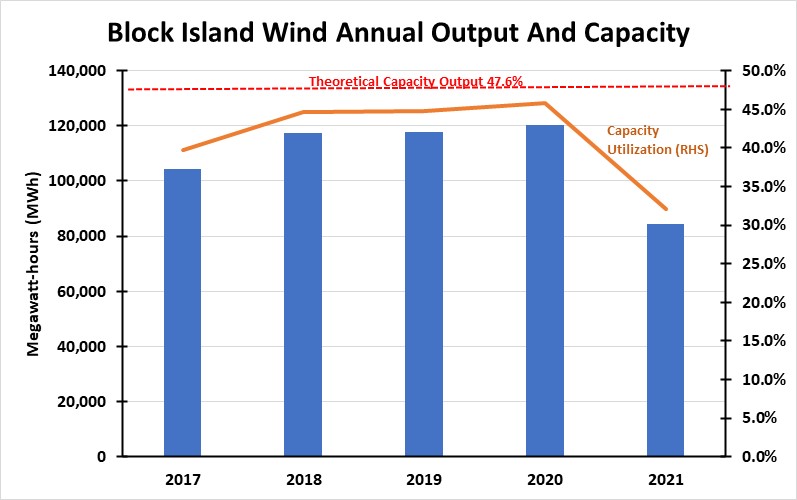

Block Island Risk Factor

The Rhode Island Public Utility Commission approved the five-turbine, 30-MW Block Island Wind farm, it was assured that 125,000 megawatt-hours (MWh) of electricity would be generated per year. Based on 365 days, this translates into a 47.6 precent utilization rate. As the chart below shows, so far in its operational history, the wind farm has yet to achieve the advertised target utilization rate in any year.

Block Island Wind Has Yet To Deliver The Power It Advertised Source: EIA, PPHB

Had a similar performance standard been mandated as proposed by Virginia’s SCC, Ørsted, the current Block Island Wind farm owner, and D.E. Shaw, the original owner, would have been on the hook for the power supply shortfalls.

Conclusion

Dominion has proposed a lower utilization rate (42.5%) than the Block Island because of the weaker winds off Virginia. The output from that project is already underperforming, and the records of other older wind farms in Europe confirm that wind farm utilization rates are often lower than initially assumed. Plus, the utilization rate declines as turbines age.

A performance standard thus protects ratepayers from electricity shortfalls.

The post Coastal Virginia Offshore Wind: Risks Aplenty ($21 billion could jump) appeared first on Master Resource.

via Master Resource

August 30, 2022 at 01:11AM