By Paul Homewood

Timera bring news that the UK’s Capacity Market Auction has been deemed to be valid by the EU, following a spurious legal challenge:

The UK capacity market was re-instated two weeks ago. This means the immediate resumption of payments for both on-going and historical capacity provided. Importantly, the European Commission found no evidence of discrimination against Demand Side Response (DSR), the claim that underpinned market suspension.

During the period of suspension, the UK government has run a separate consultation process on reforms to the capacity market. This should result in some relatively minor adjustments e.g. wind & solar are set to participate from Jan 2020 provided they receive no other support. But in summary, the capacity market is now back in play and essentially unchanged.

Reinstatement means that three auctions will now be held across the space of five weeks in Q1 2020. These will play a very important role in shaping the UK power market capacity mix into the mid-2020s.

In today’s article we look at the current UK capacity balance ‘state of play’. We also set out why we think capacity prices may surprise vs a pessimistic market consensus.

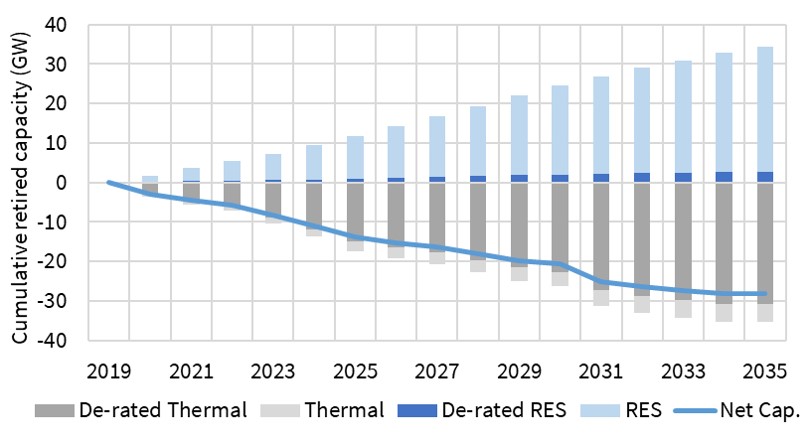

UK capacity balance: a 15 year perspective

There is a large & growing pipeline of UK wind and solar projects under development. Our scenarios are for between 25 to 30GW of aggregate nominal wind & solar capacity build across the next 10 years.

In Chart 1 we show a scenario for capacity growth from Renewable Energy Sources (RES) in the blue bars above the horizontal axis. This is broadly in line with National Grid’s Future Energy Scenarios, recognising some differences in timing and breakdown of capacity types.

But this large nominal volume shrinks to a relatively small volume once capacity is derated for intermittency. For example, 23GW of nominal RES growth by 2030 in the scenario in Chart 1 shrinks to 2GW when derated (using the latest wind & solar de-rating factors announced for the Q1 2020 auctions).

Chart 1: The net capacity deficit – RES build vs capacity closures

The grey lines below the axis in Chart 1 show a scenario for aggregate thermal retirements. This assumes:

- Coal asset closures as announced, with Drax and Ratcliffe closing by end of 2024 in line with the government’s 2025 deadline

- Nuclear plant closures as per current regulatory schedule

- CCGT closures based on major capex timing and economics of individual units.

Derating has much less impact on thermal units (e.g. CCGTs have a 90% factor vs 7% for onshore wind and 3% for solar). In the chart scenario, 23GW of derated capacity is set to come off the system by 2030.

The blue line shows the net derated capacity gap between thermal closures and RES build. These are primarily replacement volumes to be delivered via the capacity market. In other words 23GW of net closures and 1GW of RES build leaves a capacity deficit of 21GW by 2030.

That is a lot of capacity. And as things stand, it is likely to be primarily delivered in the form of gas engines, batteries, DSR and CCGTs. It is also possible that merchant RES starts to play a more important role from the mid-2020s, although still with more penal derating for intermittent sources.

Why two of the Q1 auctions are important

The T-3 auction will be held on 30th Jan 2020 for capacity delivery in the 2022-23 year (Oct – Sep). Then a T-4 auction will be held for 2023-24 delivery on 5th Mar 2020. These two auctions cover a key window of coal and CCGT closures. A ‘top up’ T-1 auction for 2020-21 will be held in between these, although today we just focus on the more important T-3 and T-4 auctions.

There is 9GW of coal capacity remaining in the UK. In 2021 this will likely fall to 3GW (i.e. Ratcliffe and 2 remaining Drax units). If the current weakness in coal generation margins (CDS) continues, this 3GW may close earlier than assumed in Chart 1 (e.g. by 2023). That could accelerate the requirement for new capacity across the Q1 auctions.

In parallel, 3-5GW of older and less flexible CCGT units are likely to close by the mid-2020s. These are mostly 1990s commissioned units that were not designed for lower load factor flexible operation and are reaching major life extension capex milestones. The level of capacity prices will influence closure timing.

These closure volumes of coal and CCGT units are creating a structural capacity deficit across the auction horizon. This means new build capacity will be required and it will likely be more expensive than in the last T-4 auction.

Capacity price pessimism vs bidding reality

One of the classic human traits that can drive investor behaviour is ‘recency bias’. We tend to place too much emphasis on recent events when making investment decisions.

In this context, the last T-1 auction clearing price (0.77 £/kW) and the last T-4 price (8.40 £/kW), shown in Chart 2, have set a tone of heightened pessimism around future capacity prices.

Chart 2: UK Capacity Auction volumes and contract price

![]()

https://timera-energy.com/uk-capacity-market-back-in-play/

The take home message is that we are likely to see the closure of 30GW of conventional capacity within the next ten years, including all the remaining coal capacity, much CCGT (particularly the older plants not designed for flexible working, and older nuclear.

A similar amount of renewable will be built, but crucially the derated capacity will be much less. (Arguably, of course, the “derated capacity should be zero”).

Even within five years, we could lose nearly 20GW.

The reinstated Capacity Market is designed to fill this gap. But the question is how much will we have to pay.

Timera reckon a price of around £20/KW/Yr may be enough, as it was in the earlier auctions, costing around £1bn a year. I believe that figure is underestimated. Previous auctions were awarded largely to existing capacity, coal, gas and nuclear. Consequently prices were kept low.

With much of that capacity due to close soon, the Auction will need to attract a tranche of new capacity. With an assumed lead time of five years, new CCGT plant will need to be successful at next year’s auctions, if sufficient capacity is to be ready by 2025.

Based on BEIS levelised costs assumptions, I calculate that the fixed/capital costs for a 1GW CCGT plant are about £90m a year. Given the uncertainties going forward, concerning carbon pricing, subsidised renewables and political threats, there is no guarantee that new gas plants will be able to operate for their full technical life (certainly without investing in CCS technology). Indeed, there is little confidence that they can even make money from selling electricity in the short term up to 2030, as subsidies to renewables prevent them from running at full capacity.

They will consequently need to cover most, if not all, of their fixed costs from the Capacity Market, via 15 year contracts. At £20/KW/Yr, a 1GW plant would only receive £20m a year.

It is also worth recalling that the proposed new Trafford CCGT plant, which won a Capacity Market subsidy of £30m a year in 2014, never got off the ground, as it could not attract finance.

My guess is that new plants will need at least double that subsidy to be worth investing in.

The Capacity Market auction runs on a cleared basis, meaning that all successful bidders receive the highest price at which the auction clears. At £40/KW, therefore, the cost to consumers would be around £2bn a year.

via NOT A LOT OF PEOPLE KNOW THAT

November 11, 2019 at 01:00PM

Reblogged this on Climate- Science.press.

LikeLike